The Strategic Shockwave of Fin Tech in Global Finance

The rise of Fin Tech represents a structural transformation of global finance rather than a superficial digital upgrade. What began as agile startups targeting payment inefficiencies has evolved into a dominant force reshaping capital allocation, risk assessment, and customer engagement. This wave of financial technology challenges entrenched banking hierarchies and redistributes influence toward data-driven platforms. Traditional institutions defend regulatory trust and systemic stability, while Fin Tech champions speed, automation, and algorithmic precision. Capital markets increasingly favor technological scalability over institutional legacy. The strategic tension is unmistakable: Fin Tech either democratizes access to finance at unprecedented scale or destabilizes long-standing safeguards. Leaders who underestimate Fin Tech misread the tectonic shift underway. The financial sector is not experiencing incremental innovation. It is undergoing structural realignment driven by intelligence, connectivity, and automation.

Fin Tech as the New Architecture of Financial Power

How Fin Tech Redefines Financial Technology Infrastructure

Fin Tech reconstructs financial infrastructure through cloud-native systems, open APIs, and modular ecosystems that replace rigid legacy cores. Traditional banking technology was built for stability, not agility, resulting in costly maintenance and slow product iteration. Fin Tech platforms operate through continuous deployment models that enable rapid feature enhancement and seamless integration across services. The World Economic Forum highlights this transformation in its analysis of the digital transformation of financial services ecosystems

https://www.weforum.org/agenda/archive/financial-and-monetary-systems/

Fin Tech firms function as adaptive networks rather than static institutions, positioning financial technology as a dynamic engine of market responsiveness and structural competitiveness.

Traditional Banking vs Fin Tech Infrastructure

| Dimension | Traditional Banking | Fin Tech Model |

| Core Systems | Legacy, monolithic | Cloud-native, modular |

| Innovation Speed | Slow release cycles | Continuous deployment |

| Customer Access | Branch-centric | Mobile-first |

| Integration | Closed systems | Open APIs |

Why Fin Tech and AI Are Accelerating Financial Autonomy

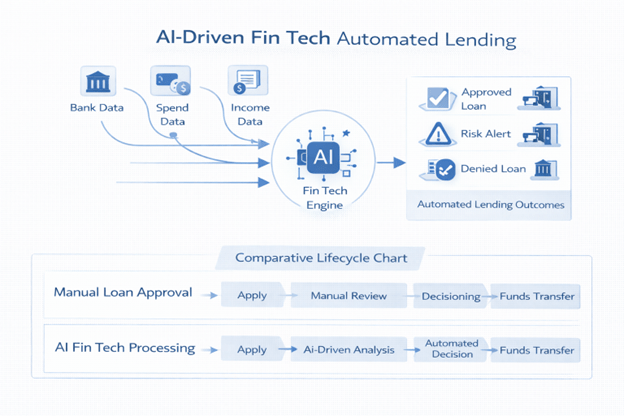

Automation is the decisive multiplier behind Fin Tech expansion. The convergence of fintech and AI enables predictive modeling, automated underwriting, intelligent fraud detection, and dynamic pricing systems that continuously learn from data inputs. These capabilities reduce human bias while dramatically accelerating decision cycles. As explored by MIT Technology Review in its coverage of AI transforming financial services

Fin Tech platforms integrate behavioral analytics and transaction histories to create self-optimizing ecosystems. Financial autonomy becomes algorithmically enhanced rather than institutionally constrained, empowering users while reshaping competitive advantage.

Fin Tech vs Traditional Banking: Efficiency or Systemic Instability?

How Fin Tech Challenges Legacy Banking Models

Fin Tech aggressively targets operational inefficiencies embedded within traditional banking models. Conventional institutions rely on bureaucratic approval hierarchies, physical branch networks, and fragmented data silos that slow responsiveness and inflate operational costs. Fin Tech firms streamline onboarding, payments, and lending into unified digital journeys optimized for speed and scale. McKinsey documents this operational shift in its research on the future of digital banking transformation

The contrast is structural rather than cosmetic. Financial technology eliminates friction at every customer touchpoint, redefining expectations for immediacy and accessibility.

Key Operational Differences:

- Instant digital identity verification

- Real-time transaction monitoring

- Automated compliance screening

- Continuous behavioral analytics

Can Traditional Institutions Survive the Fin Tech Disruption?

The defense of legacy banking centers on capital adequacy, regulatory relationships, and historical trust. Yet Fin Tech firms increasingly secure licenses, expand lending portfolios, and embed compliance into their technological architecture. Survival depends on strategic integration rather than institutional pride. Banks that collaborate with financial technology partners enhance agility while retaining balance-sheet strength. Those that resist transformation risk erosion of relevance. The disruption is not speculative. It is operational. Strategic alignment with Fin Tech ecosystems determines whether traditional institutions evolve into hybrid innovators or decline into infrastructural relics.

Strategic Responses to Fin Tech Disruption

| Strategy | Risk Level | Long-Term Viability |

| Ignore Fin Tech | High | Decline |

| Compete Directly | Medium | Uncertain |

| Partner with Fin Tech | Low | Sustainable Growth |

| Acquire Fin Tech Firms | Medium | Accelerated Transformation |

Fin Tech and AI: Intelligence, Automation, and the Death of Manual Banking

Fin Tech and AI in Risk Modeling and Credit Decisions

Fin Tech transforms intelligence in finance by embedding machine learning directly into risk modeling frameworks. Traditional credit scoring relies heavily on historical financial behavior and rigid criteria. Fintech and AI systems analyze alternative datasets including transaction patterns, behavioral signals, and contextual indicators. Harvard Business Review explores how algorithmic decision systems enhance business forecasting and risk management

Adaptive learning continuously refines predictions, improving inclusion while reducing inefficiencies. Manual underwriting becomes strategically obsolete when algorithms update in real time across dynamic market conditions.

Ethical Risks of Fin Tech and AI Automation

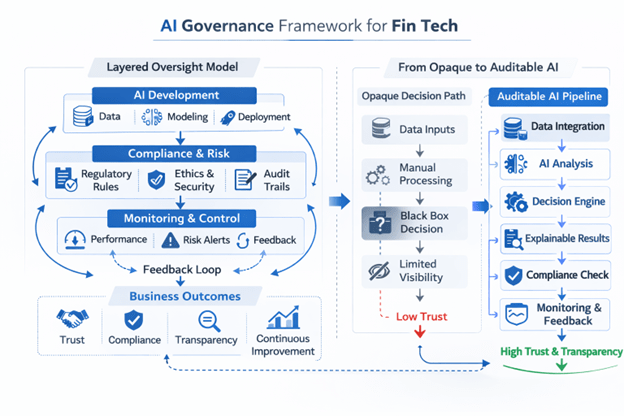

Critics argue that Fin Tech automation introduces opacity and algorithmic bias into financial decision-making. Without governance frameworks, AI-driven models may replicate structural inequalities embedded within training data. However, responsible oversight mechanisms can mitigate these risks. Deloitte outlines structured governance approaches in its research on responsible AI and ethical risk management in financial services

Transparency, auditability, and human supervision transform AI from a liability into a strategic safeguard. The danger lies not in automation itself, but in unmanaged deployment.

Fin Tech Investment Surge: Innovation Boom or Speculative Bubble?

The Rise of Financial Technology Partners and Venture Capital

Investment momentum behind Fin Tech reflects structural demand rather than speculative hype. Venture capital continues to fuel innovation across digital payments, decentralized finance, and AI-enabled lending platforms. Strategic alliances with financial technology partners accelerate ecosystem expansion and operational scalability. IBM emphasizes the strategic value of platform ecosystems in its analysis of digital transformation in financial services

Capital markets recognize that financial technology is reshaping competitive moats. Funding flows toward scalable intelligence, not toward incremental improvements of legacy infrastructure.

Consolidation Trends in Fin Tech Markets

Rapid growth inevitably leads to consolidation within the Fin Tech sector. As product categories mature, competitive pressures drive mergers, acquisitions, and strategic integrations. Smaller firms often specialize in niche capabilities that larger platforms absorb to expand service portfolios. This consolidation phase mirrors previous technological revolutions where fragmentation precedes structural stabilization. Financial technology ecosystems become more resilient through integration. Market concentration does not signify decline. It indicates maturation. Fin Tech’s trajectory suggests durable infrastructure rather than transient experimentation.

Regulatory Tension: Will Fin Tech Be Controlled or Empowered?

Global Regulatory Responses to Fin Tech Expansion

Regulators confront a strategic dilemma regarding Fin Tech expansion. Excessive control may suppress innovation and reduce competitive dynamism. Insufficient oversight risks systemic vulnerabilities. The World Economic Forum advocates adaptive governance in its initiative on shaping the future of financial and monetary systems

The regulatory landscape is shifting toward iterative frameworks that evolve alongside technological progress. Fin Tech requires structured flexibility rather than rigid constraint. Policy that adapts can protect stability while fostering digital acceleration.

Compliance Technology as a Fin Tech Growth Engine

Compliance is no longer a bureaucratic burden within Fin Tech ecosystems. It becomes an innovation catalyst. Automated monitoring systems, real-time reporting, and identity verification tools integrate directly into digital platforms. McKinsey highlights how regtech solutions strengthen resilience and efficiency

These technologies transform oversight into a competitive advantage.

Drivers of Compliance-Led Growth:

- Automated regulatory reporting

- Continuous transaction analytics

- Integrated identity verification

- Dynamic risk exposure modeling

Fin Tech demonstrates that structured compliance enhances scalability rather than restricting it.

Fin Tech Customer Experience: Empowerment or Illusion of Control?

Hyper-Personalization Through Fin Tech and AI

Customer experience represents the most visible advantage of Fin Tech. AI-driven personalization engines analyze spending patterns, investment behaviors, and financial goals to tailor recommendations dynamically. Harvard Business Review examines the strategic implications of AI-driven customer personalization

Financial services shift from static product offerings to adaptive ecosystems that respond to user behavior in real time. Hyper-personalization increases engagement while redefining expectations for immediacy, transparency, and financial autonomy.

Data Ownership and Privacy in Fin Tech Ecosystems

Data fuels Fin Tech dominance, yet it also generates strategic tension around ownership and privacy. Continuous data capture enhances predictive accuracy but raises concerns regarding surveillance and consent. Transparent governance models and encryption architectures determine competitive differentiation. Deloitte underscores the importance of data governance and privacy frameworks in digital transformation

Fin Tech platforms that embed privacy into design gain institutional trust while sustaining innovation velocity. Responsible data stewardship strengthens, rather than limits, technological advantage.

Fin Tech’s Verdict on Traditional Banking: Evolution or Extinction?

The strategic verdict is decisive. Fin Tech is not an experimental overlay on traditional banking. It is the evolutionary pathway of finance itself. Institutions that integrate financial technology and collaborate with financial technology partners position themselves for sustained relevance. Those that resist automation and intelligence risk gradual erosion. AI-enabled Fin Tech optimizes capital flows, enhances inclusion, and accelerates decision-making cycles across markets. Regulation will mature, consolidation will stabilize volatility, and governance frameworks will strengthen oversight. The transformation will not reverse. Finance without Fin Tech signals institutional stagnation. Finance empowered by intelligent systems signals competitive acceleration. The future belongs to organizations that adopt technological architecture as their strategic core. Adaptation secures growth. Resistance guarantees decline.

References

World Economic Forum – Digital Transformation of Financial Services Ecosystems

MIT Technology Review – Artificial Intelligence in Financial Services

McKinsey – The Future of Digital Banking Transformation

Harvard Business Review – Artificial Intelligence and Business Strategy

Deloitte – Responsible AI in Financial Services

IBM – Digital Transformation in Financial Services

McKinsey – RegTech and Risk Resilience Insights

Harvard Business Review – Customer Experience and AI Personalization

Deloitte – Data Privacy and Governance in Digital Transformation

H-in-Q – Fin Tech Wallets: Control, Convenience or Complacency?